Consumers take on debt counsellors

Credit watchdog rules in consumer's favour on prescribed debt, excessive interest, fraud and credit insurance

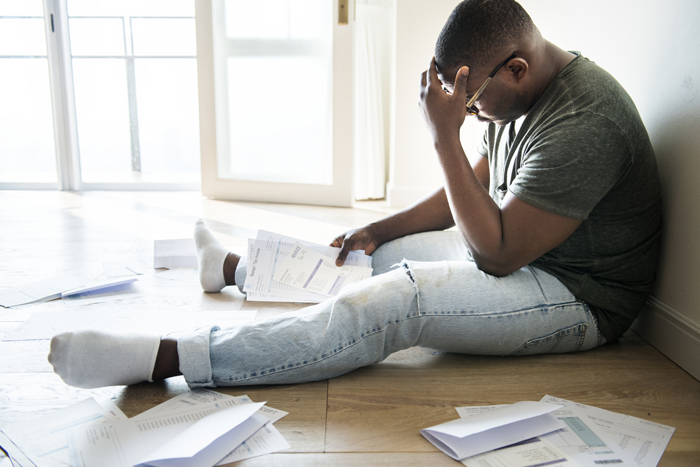

Complaints about debt counselling and debt counsellors top the list of grievances received by the office of the Credit Ombud.

Complaints about debt counselling and debt counsellors make up a significant number of grievances received by the office of the Credit Ombud, the ombud’s latest annual report shows.

Last year, the Credit Ombud received 2,239 complaints about debt counselling and 782 complaints against debt counsellors, interim ombud Howard Gabriels told Money. Since the Credit Ombud does not have jurisdiction in these matters, these complaints are referred to the National Credit Regulator (NCR).

Gabriels says the fact that 10% of all complaints received by his office relate to debt counselling is indicative of the pressure consumers are under due to tough economic circumstances.

He says debt counselling-related complaints included, but were not limited to:

- The costs and fees that apply;

- How accounts are administered in the process;

- The delays and backlogs in finalising the process;

- Disputes relating to debt restructuring proposals and the acceptance of proposals made; and

- Failure to update the consumer’s credit profile once the process had been completed.

The largest category of complaints to the Credit Ombud last year was credit information disputes, which accounted for 45% of complaints received.

Gabriels says his office, which is mandated to resolve both non-bank credit and credit information disputes, found in favour of consumers who had complained about incomplete, incorrect and outdated data on their credit profiles, as well as those with debts that had prescribed and those with fraudulent accounts reflecting on their credit reports.

The Credit Ombud recovered R6.9m for consumers last year, compared with R8.3m in 2018 (and R15.5m in 2017), and the percentage of complaints settled in favour of consumers also dropped to 57% last year from 61% in 2018.

While the number of complaints and enquiries increased last year by 3,445 compared with the previous year, there was a decrease in the number of disputes opened and closed. Last year, the ombud’s office opened 673 fewer disputes and closed 510 fewer disputes than the year before.

The average time it took the ombud’s office to resolve a dispute was 43 days, which is an improvement on the previous year, when it took almost 50 days.

The annual report notes a drop in customer satisfaction, from 87% to 80%. Gabriels says this can be attributed in part to the fact that his office is no longer dealing with credit-related complaints about banks, leaving consumers disgruntled that they weren’t able to receive assistance.

The Banking Association of South Africa decided it would be more practical for the Banking Ombud to deal with all bank disputes and terminated the banks’ membership of the Credit Ombud with effect from 1 October last year.

Gabriels says complaints relating to banks made up a total of 25% of all complaints.

The withdrawal of the banks put financial strain on the organisation, resulting in retrenchments and reining in expenditure.

In the annual report, Lee Soobrathi, the head of case management and dispute resolution, provides the following case studies illustrating the type of disputes resolved:

Notice prior to default listing

A consumer complained to the Credit Ombud’s office that her credit provider did not give her notice prior to listing a default on her credit report. An investigation revealed that the notice provided was defective and warranted the removal of the default listing.

Prescribed debt

A consumer claimed that a loan account reflecting on his credit report had prescribed. The credit agreement was sold to a third party which continued to try and collect on the outstanding balance. Upon investigation, prescription was confirmed, and the account closed. This resulted in a write-off in the amount of R6,630.

Excessive interest charges

A consumer disputed the outstanding balance on his account claiming that the credit provider had been overcharging on interest and fees. Upon investigation it was found that the interest charged was in breach of Section 103(5) of the National Credit Act. The account was adjusted, resulting in a refund to the value of R1,686.

Credit insurance

A consumer’s claim for retrenchment cover under his credit agreement was short paid. The complaint was resolved in favour of the consumer with the provider paying out a further R12,579 to the consumer.

Fraud

A consumer disputed purchases made on his account with a credit provider, claiming that these purchases were fraudulent transactions. Upon investigation fraud was confirmed, and transactions to the value of R20,983 were reversed.

Cancellation of credit agreement

A consumer terminated her credit agreement with the credit provider. The account continued to reflect as due and payable on her credit profile at the credit bureau, which prevented her from successfully applying for credit with other credit providers. An investigation by the Credit Ombud revealed that the account was in fact cancelled and the credit bureau was asked to update its records.