15 things you need to know about debt relief

Strict conditions on who will qualify

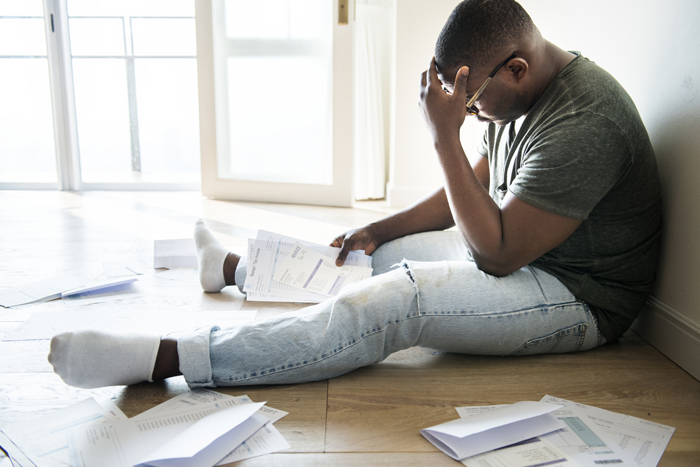

If you’re expecting to have your debts written off now that the debt relief bill has been signed into law, don’t.

If you’re expecting to have your debts written off now that the debt relief bill has been signed into law, don’t.

There’s no commencement date for the controversial legislation, and even if applications were open and you were found to be eligible for it, you won’t necessarily have your debts extinguished or even suspended.

Instead, you might be placed in a form of debt review administered by the National Credit Regulator (NCR).

The debt relief intervention that forms part of an amendment to the National Credit Act seeks to help you if you are overindebted, earn less than R7,500 a month and have unsecured debt of no more than R50,000.

This is what you need to know about it:

- If you are in debt counselling, have been sequestrated or have an administration order, you don’t qualify for debt intervention.

- Applications for debt intervention will be processed by the NRC and then submitted to the National Consumer Tribunal (NCT). But the NCR isn’t ready yet to even start processing applications.

- The writing-off or extinguishing of debt is a last resort. Riccardo Petersen, a director at law firm Norton Rose Fulbright, says that in many instances, a long process would precede a decision by the tribunal to write off your debts.

- The NCR will first assess whether you could pay off your debts by way of a debt rearrangement. This means you get to pay a lesser instalment over an extended period of no more than five years. This is similar to debt counselling, except you would not have to pay a debt counsellor nor enjoy the services of one.

- If you have no income, the regulator will recommend that your debts be suspended for 24 months in the hopes that your circumstances will change and you will be able to satisfy your debts in time. During this time interest and fees stop running, says Nthupang Magolego, a legal adviser at the NCR.

- If your circumstances improve at any point during this period and you could pay off your debts via debt rearrangement, the regulator will make this recommendation to the tribunal, Magolego says.

- You will be required to attend a financial literacy programme provided by the NCR, which is aimed at rehabilitating you as a consumer of credit.

- If after 24 months there has been no improvement in your circumstances, like your employment status, only then will the regulator apply to the tribunal for your debts to be written off.

- If you apply for debt relief you may not enter into any more credit agreements, other than a consolidation loan. That is unless your application was rejected, you were found to be not over-indebted or you have fulfilled the re-arrangement agreement, say Trudie Broekmann, an attorney who specialises in consumer law.

- Your creditors may not take legal action against you unless your debt relief application is rejected or you default on a rearrangement agreement, she says.

- If a credit provider enters into a credit agreement with you (other than a consolidation loan), all or part of the credit can be declared reckless.

- If you enter into a credit agreement while enjoying the benefits of debt relief, debt relief will not apply to that agreement.

- If a credit agreement is extinguished under debt relief, the credit provider may not enforce any right under that agreement.

- If you furnish false information when applying for debt relief, you can be fined or imprisoned for not longer than two years, or both, and are permanently prohibited from applying for debt relief.

- If your application for debt relief is rejected, you may approach the magistrate court to rearrange your credit agreement obligations.

Magolego says that the extinguishing of debt will take place for a limited period of 48 months only, after which there will be an impact assessment to determine its efficacy and whether or not it should become a permanent feature of the law.